Эрдсийг эрдэнэст

Ирээдүйг өндөр хөгжилд

Ирээдүйг өндөр хөгжилд

Mining The Resources

Minding the future

Minding the future

The Mongolian Mining Journal /May 2020/

By E. Odjargal

Banking reforms would have to wait. The Spring session of the present Parliament, its last before members to its successor are elected, ended without completing discussions on them, presented as part of an economic package. Members of the Government were keen to make some progress on the reforms, and so was the IMF as part of its Extended Fund Facility package, but time was against them.

The ante was being upped even before the session began, with Prime Minister U. Khurelsukh saying on 27 March that the time was ripe to change the way the country’s commercial banks worked, warning that “if banks don’t accept our suggestion to reduce their lending rates, we shall have to take stern measures to see that this is done.” Finance Minister Ch. Khurelbaatar followed this up on 14 April, when he said in Parliament that after two years of calling for banking sector reforms and asking for Parliament’s permission to let foreign banks work in Mongolia, the Government now wanted to get the required laws passed without delay and thus “put a stop to the monopoly of the commercial banks”. Earlier, in his speech to open the spring session on 5 April Speaker G. Zandanshatar had revealed that banking reforms were a major part of the package of economic measures the Government would be submitting for Parliament’s approval.

The ruling MPP had earlier set up a team to suggest amendments to the existing laws that would make banks work in a more transparent manner and allow more shareholders into their closed ownership structure. Among the other things sought to be achieved through the amendments were: quick disposal of customers’ claims from banks that declare bankruptcy; setting a limit of 20% on an individual’s shareholding in a bank; lower interest rates on consumer loans; digitalization, etc. As an example, the group suggested that the current interest rate of 15%-20% on consumer loans up to MNT500 million could be brought down by 8 percent if the banks charged 3% less and the government gave another 5% exemption.

The Extended Fund Facility Program of the IMF ending this month called for, along with other things, a rehabilitation – a euphemism for reform – of Mongolia’s banking system. Progress on this has been tardy, as we have shown, with the result that the IMF has not released the last tranche of its promised funds.

Earlier during the programme, the IMF made an assessment of the asset quality of commercial banks, and found that seven of them had inadequate capital. One of them, Capital Bank, soon after announced its bankruptcy, and the other six were given until end of 2018 to increase their capital reserve. After a verification audit in September 2019 had found that some of the six still did not have enough reserves, the IMF gave them time until the end of 2019 to mend matters. An IMF team was scheduled to visit Mongolia in April to assess their compliance as part of the implementation of the EFF program, but it could not come because of the coronavirus outbreak.

We describe below what major players in the banking sector have done and faced in the last four years, and what the policy and decisions on the sector have been of the government which has been in power during this period and which has been pressing for banking reforms.

The Bank of Mongolia

While most of its senior executives are appointed for a period of 4 years, which corresponds to the term of the appointing government, the Governor of the Bank of Mongolia is selected by Parliament for a 6-year term. The present government appointed its first Governor soon after coming to power in 2016 and he lost little time in starting work on fresh laws and on amendments to existing laws to regulate the banking sector. In two years the central bank prepared drafts of 11 laws. These were discussed in parliament and among those that were adopted are Law on the Central Bank, Law on Banking, Law on Insurance of Monetary Deposits in Banks, Law on National Payment System, and Law on Eradicating Money Laundering and Terrorist Financing. This means the principal laws in the banking sector were amended. Ironically he had to leave after FATF, an international organization, had put Mongolia on its “grey list” for having failed to adequately comply with its earlier recommendations concerning anti-money laundering and counter-terrorism financing measures. His successor in the job now has the twin responsibilities of taking Mongolia out of the “grey list” and of framing and implementing monetary policy to keep the economy stable at the time of the COVID-19 crisis.

The main feature of the present monetary policy has been a gradual lowering of its policy interest rate. This now stands at 9 percent, the lowest in five years. In addition, the minimum mandatory cash reserve in commercial banks has been reduced twice since 2018, first to 10.5 percent and then again to 8.5 percent. This last was in March when the Coronavirus situation was threatening the economy from all sides. The move has given the banks access to an additional MNT300 billion. This can be given out as loans and it also allows them to reduce loans repayment rates.

The Development Bank

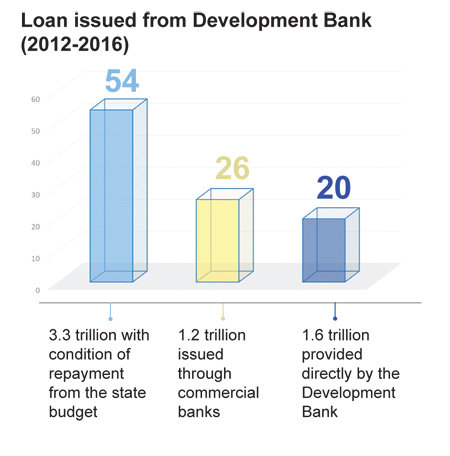

The Development Bank was established nine years ago specifically to finance important development projects and programmes of strategic importance supporting economic growth. However, it has not been able to fulfil its promise because of lack of funds, after 85.2 percent of its total capital was spent on granting loans, most of which awaits repayment, and may have to be written off. Soon after coming to power in 2016, the present Government set up a team to report on all financial transactions by the bank since its inception, including the loans so far issued, and to detail how recipient projects had been selected, how much of the amounts borrowed had been spent on what, and the progress of their implementation.

The team’s report highlighted that most of the projects were in the name of people from both the DP and the MPP, many of them members of parliament, now or earlier.

From the graph below, it is clearly seen that the terms of the loan agreement for more than half of the projects are that repayment would be made from the state budget, which means taxpayers’ money would be used to finance dubious projects. After the audit the loans were transferred to the Finance Ministry at the end of 2016.

State-owned companies have taken 59 percent of the direct loans issued by The Development Bank, with the mining sector accounting for nine of the 16 larger projects. Successive Parliament and Government Resolutions have since led to all these 16 loan agreements to be amended. The loan of the New Railway Project of the state-owned Mongolian Railway has been transferred to the Government.

The Central Geological Laboratory, a state-owned enterprise, and Erdenes Tavantolgoi and Baganuur, both joint stock companies, have fully repaid their loans. The Development Bank signed sub-loan agreements with 11 banks for loans totalling MNT 1.2 trillion, 60 percent of which was granted through Golomt Bank and Trade and Development Bank. There is uncertainty about the outstanding loan to Capital Bank, which has declared bankruptcy.

Parliament amended the Law on the Development Bank on February 10, 2017 and three months later appointed G. Amartuvshin as its CEO. There has been no satisfactory explanation of why he resigned after only six months, especially as this coincided with the dismissal of the Governor of the Bank of Mongolia.

Commercial banks and mining

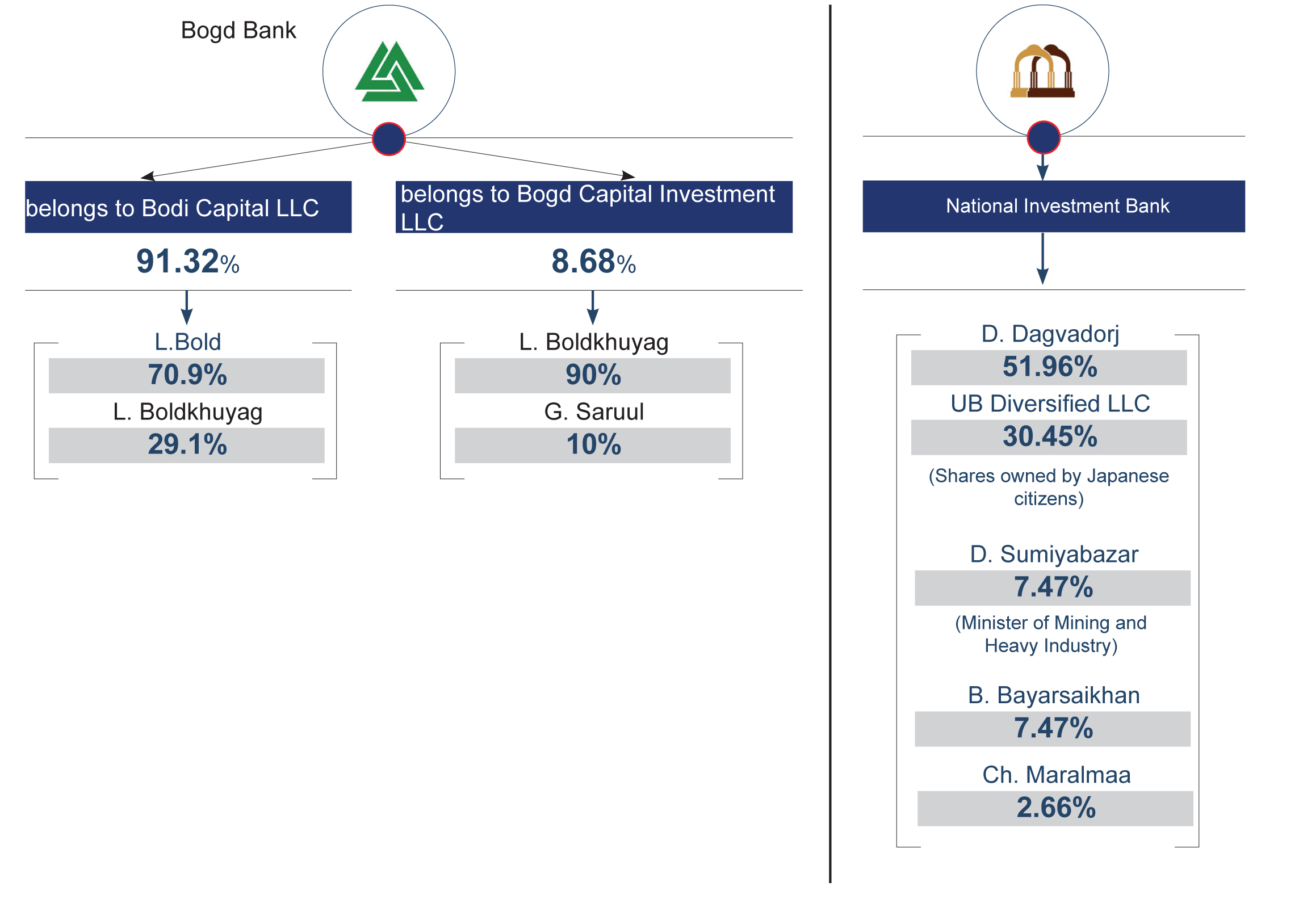

There are now 13 commercial banks operating in Mongolia, all registered as a limited liability company. Five out of them have foreign shareholders, including companies registered abroad. Two Mongolian MPs have significant shares in two banks -- D. Sumiyabazar, who is also Minister of Mining and Heavy Industry, and L. Bold.

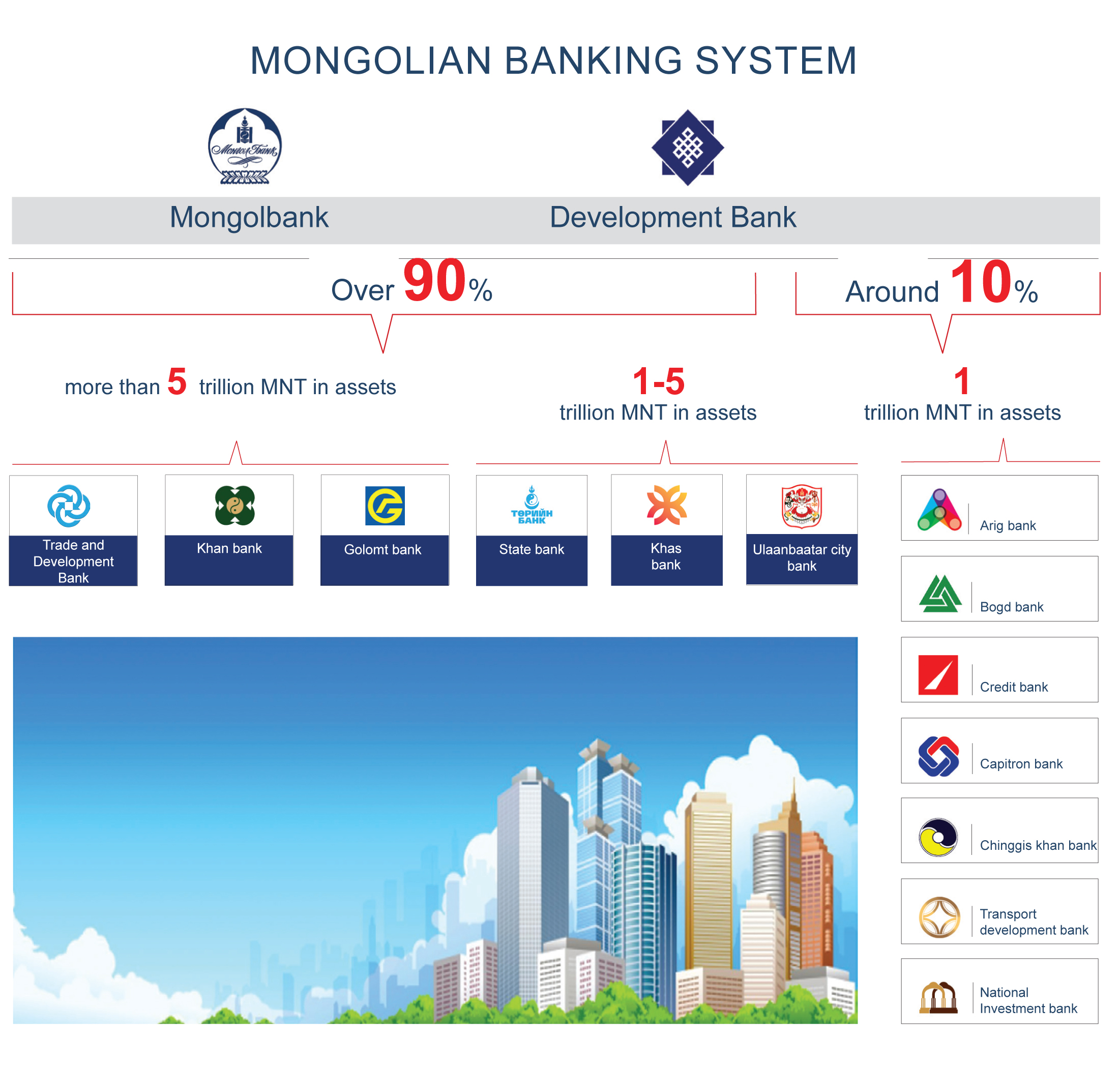

According to the Bank of Mongolia, Trade and Development Bank, Khaan Bank, Golomt Bank, Khas Bank, State Bank, and Ulaanbaatar City Bank together account for more than 90% of the total banking space. At the end of 2019, the total assets of the 13 banks stood at MNT32.7 trillion, showing a year-on-year growth of 10% for the large and medium banks, and of 13% for the small banks.

The Centre for Economic Policy and Competitiveness Study classifies banks as large, medium and small on the basis of their monetary worth, after comparing indicators such as assets, loans, deposits in current and savings accounts and profits, as these appear in their financial summary reports.

Last year, the commercial banks together posted after-tax profits of MNT386 billion. MNT337 billion of this was made by the large banks and MNT29 billion by the medium banks, while the small banks lost money, as they have done in the last years.

A bank’s main source of income is the interest it earns from loans. The total lending by all banks to economic entities, organizations and individuals stood at MNT18.1 trillion at the end of 2019, showing a 45.7 percent growth over the figure for 2016. Loans to individuals made up 52.1 percent of the total and the remaining 47.9 percent went to companies and organizations. The amount of non-performing loans increased by 73.5 percent in the last three years. The amount of loans granted to the mining and extractive industry has been rising every year constantly since 2010 but so has that of non-performing loans.

In 2019, over MNT500 billion or 34 percent of the total MNT1.5 trillion going to mining and extractive units was shown as non-performing loans. This was despite the fact that the economy had been growing and the price of raw materials had been stable since 2016. There is every risk that as a result of the COVID-19 crisis throughout the world banks will see more cases of non-repayment and an increase in the number of non-performing loans.

Several incidents concerning commercial banks have claimed popular attention during the term of the current parliament, and not all of them for reasons related to professional banking. Two of them are remembered below.

The Trade and Development Bank and 49% of Erdenet

Almost overlapping the days of the 2016 election came the announcement that a Russian company’s 49 percent stake in Erdenet Mining Corporation and MongolRosTsvetMet had been bought by a little-known Mongolian company for $400 million. Any joy that the iconic Erdenet was now totally owned by Mongolians was short-lived, giving way to suspicion about the bona fides of the deal. The revelation that the Trade and Development Bank had lent the money to Mongolian Copper Corporation to buy the stake merely added to the controversy.

The Trade and Development Bank had earlier also financed large and landmark projects, such as equipment renovation by the Mongolian Railway, adding to the assets of Erdenet Mining Corporation, and purchase of Mongolia’s first Boeing aircraft. It had also raised $500 million at the international market. Thus the admission of O.Orkhon, CEO of the bank, that it had had a role in clinching the deal between Rostech and Mongolian Copper Corporation besides lending a large sum to the latter, should have been no surprise but, instead, people wondered why it had involved itself in negotiations on such a sensitive issue and whether it had the legal sanction to advance so much money on an international deal.

The legality and also the legitimacy of the deal are still to be finally resolved. Meanwhile, the Mongolian Government, citing a Parliament Resolution, has taken into state ownership the disputed shares of Erdenet Corporation and Mongol RosTsvetMet, making both 100 percent state-owned. Nothing has been heard of the status of the loan from TDB to Mongolian Copper Corporation.

The Salkhit bond as an instrument of payment

After its announcement that all pension-backed loans taken by the elderly were to be written off, the government was faced with the problem of how to reimburse the banks which had lent out the MNT757.9 billion. It was decided to pay them through bonds at 6% interest redeemable after five years with money to be earned from sale of silver from the Salkhit deposit. As holder of the licence of the silver mine, Erdenes Mongol issued closed bonds of MNT900 billion and deposited them with, the State Bank, the Trade and Development Bank, Ulaanbaatar City Bank, National Investment Bank, Khaan Bank, Golomt Bank, Chinggis Khaan Bank and Capitron Bank. Each bank now holds bonds whose value is proportionate to its part of the total amount of the loans that were written off. As the biggest lender, Khaan Bank holds 66.3 percent, followed by the State Bank with 23 percent, with the rest divided among the other six banks.

Many were surprised at this novel way the Government chose to meet its obligations but possibly more surprising was the easy acquiescence of the Development Bank to stand guarantee for redemption of the bonds. Since production at the Salkhit deposit is yet to start, income from sale of its silver is, to say the least, uncertain. If that indeed turns out to be so, then it will be the people paying for a populist pre-election decision.

No matter what its real priorities are, as distinct from pre-election posturing and tall talk, the new government would find it prudent not to proceed with baking reforms early on. This is because the economic situation following the coronavirus quarantine finds banks in disarray. Borrowers are not able to repay and relief measures announced by the Bank of Mongolia – such as reducing its policy interest rate to 9 percent and allowing commercial banks to operate with a lower amount of capital – have not had much impact. Things continue to be uncertain but are unlikely to get better with Mongolian banks. It might not be sensible to impose reforms on struggling banks, though deposits must be safeguarded.