Эрдсийг эрдэнэст

Ирээдүйг өндөр хөгжилд

Ирээдүйг өндөр хөгжилд

Mining The Resources

Minding the future

Minding the future

B.Tugsbilegt

We have often noted how the US-China “trade war” can, even if obliquely, affect Mongolia’s exports to its southern neighbour, but just when the two countries announced a truce in mid-January and raised hopes of smooth sailing in the new year, came news of an unexpected threat – the coronavirus. The infection from this virus, almost crippling life in China and threatening to spread worldwide, is endangering the global economy, and nearer home, Mongolia’s trade with its biggest and almost sole export destination.

When coronavirus cases in China were first reported in December 2019, nobody elsewhere took much notice. Many recalled the SARS scare of 2003 but forgot that at that time China’s share of the global economy was just 4.3%, and this has now surged to around 19%. If that big an economy suffers a big shock, the ripples would be felt everywhere. And that is exactly what is happening. Commodity prices are falling and it is feared the Chinese economy could end the first quarter of the year with 0 percent growth.

This is alarming for Mongolia as 90 percent of our total export last year was to China, which was also where 34 percent of our total import originated. As the virus spread in the beginning of February, several countries started to restrict their trade with China. Such loss of trade could hit Australia very badly, but Mongolia could suffer more from Chinese slowdown. The Finance Ministry and the central bank are now working on estimating how much the Mongolian economy would likely be impacted. Much would depend on how quickly the virus is tamed and how fast and how well China recovers from the blow.

At the time of writing this, the ban on coal export imposed by The State Emergency Commission on February 10 is to last until March 2. Actually, the major exporters, including MAK and SGS, had stopped shipments at the end of January itself. J. Zoljargal, CEO of Mongolian Coal Association, rued that export would well have continued if we had a coal railway. As it is, with the virus rampant in China, the Mongolian coal sector is forced to wear masks.

In February 2019 Mongolia exported around two million tonnes of coal for $163 million. That gives an idea of what the present halt is going to cost us. Even though Oyu Tolgoi exports through Gashuunsukhait continue to be normal, coal is now our main export commodity, and the loss of revenue can go beyond being considerable. The Finance Ministry may well have to amend the budget, and is at present closely watching how things develop. It can afford to wait as under the law, an amendment is necessary only when revenue shortfall reaches 3% of GDP. Since GDP is put at MNT37 trillion, action would be called for only when the budget revenue falls by approximately MNT1 trillion. We all hope that the doomsayers who say the international economic impact of the coronavirus shock would be even worse than the 2008-2009 global financial crisis will be proved wrong, and it would be limited to being a short-term one, something that the Mongolian economy can absorb without being crippled.

As the market shrinks, the prices of copper, oil, and iron ore are the ones that have fallen the most. China accounts for 50 percent of the global copper demand, so it is no surprise that the LME copper price is down to $5600-$5700 per tonne from $6200. Our budget assumption was that the average copper price would be almost $6000/t. As for coking coal, the price of the Australian premium variety has not fallen but this is in a way because Chinese domestic output continues to be low.

Even if the effects of coronavirus are neutralised soon, how quickly would China recover and Mongolian coal export resume? There is reason to be optimistic as, after the SARS-induced slowdown in April and May 2003, the Chinese economy recovered enough and quickly enough to post a high growth rate at the end of the year. China’s central bank interest rate is now at around 4 percent, which indicates there is no undue panic.

Meanwhile, the US$ continues to grow stronger against the MNT, surprisingly so if we look at some fundamentals. For example, in recent years our exports have been regularly scaling record high levels, and in 2019 the balance of payment was positive, standing at $452 million. With support from the IMF programme, our foreign exchange reserves have increased dramatically. But the US$-MNT exchange rate gives another picture. When the IMF Extended Fund Facility was approved in May 2017, US$1 was MNT2411 but this kept on rising and reached MNT2679 in October 2019, when FATF put Mongolia on its ‘gray list’. In the four months since then, the MNT has fallen to 2750 against the US$, showing an average daily drop by MNT0.66. The only reason for this anomaly is the people’s lack of confidence in the sustainable long-term strength of the MNT, a feeling that persuades them to ignore the growing strength of the economic fundamentals. Economists are not surprised that popular psychology overrules statistics.

But are the authorities doing enough? When forex reserves stood at a historic high of $4.35 billion at the end of 2019, the central bank said it would hold the exchange rate stable. It did not or rather it could not because the government had other ideas. It is now clear that the President’s decision to write off pension-backed loans was actually meant to release a huge amount of cash into the market. That would mean more inflation, and further weakening of the MNT, but since the money would be raised through sale of bonds, the forex reserves would not be touched, at least for now. That he promises to redeem the bonds with revenue from sale of silver from Salkhit, a mine that has not yet started extraction, is neither here nor there when you think politically.

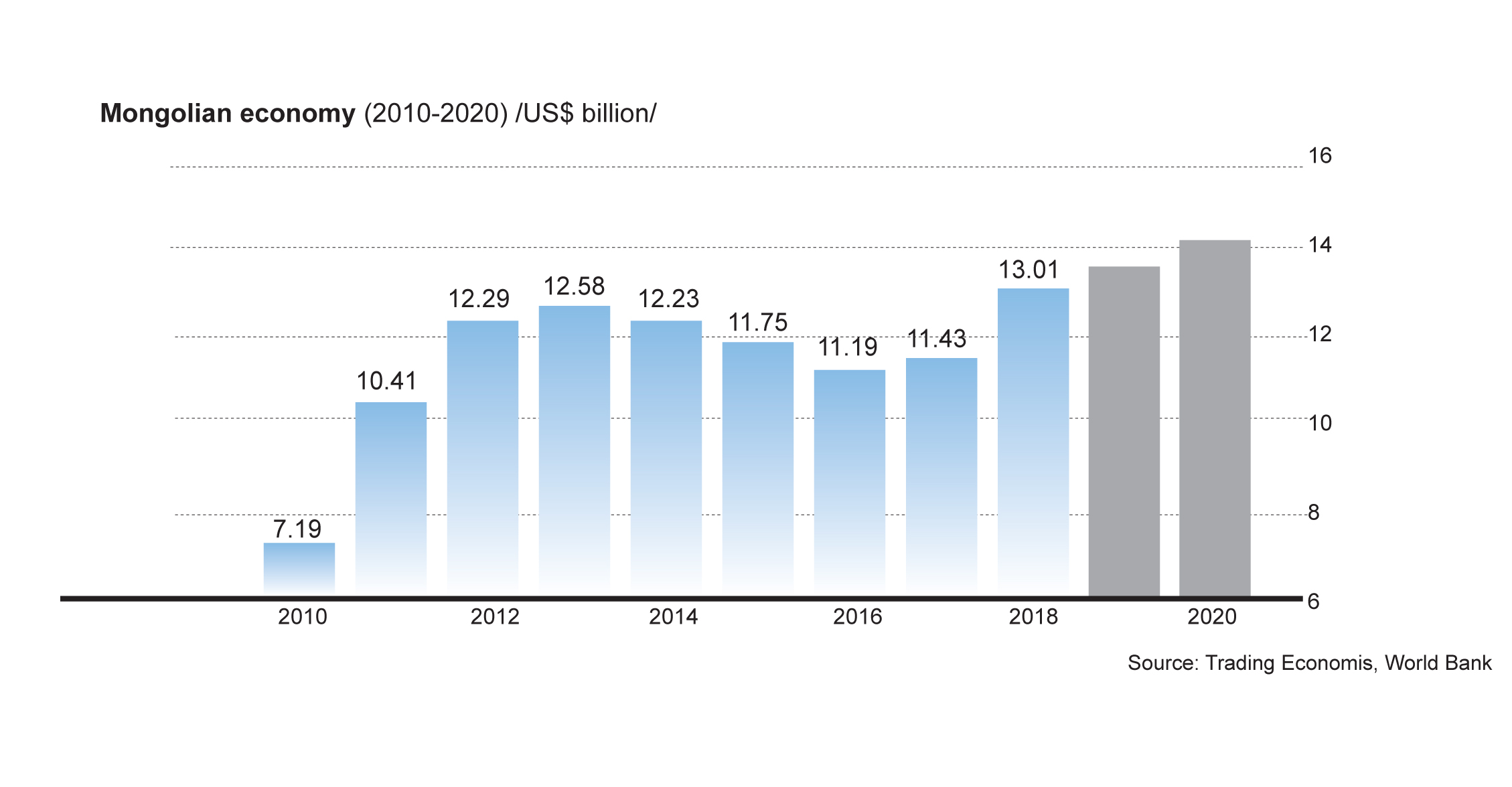

When we pay more for a dollar, it means that even when the economy looks bigger in MNT terms, it is stuck at the same point, if not made smaller, when expressed in dollars. That is why Mongolia is said to have a ‘vacuum economy’. According to the National Statistics Office, our GDP was MNT16.6 trillion in 2012 and almost MNT37 trillion in 2019. That is almost a 250% rise, but expressed in US$ terms, this GDP was $12.3 billion in 2012 and $13.6 billion last year, quite a small increase. The significant rise in the MNT figures has been neutralized by the simple fact that in 2012 $1 was MNT1300-MNT1400 but last year it surged above MNT2700. In other words, if the MNT was stable, our economy could be twice the size it is now.

Whatever the impact of coronavirus might be, there is no uncertainty about the following: We have big debts and these must be repaid on time; the IMF programme has helped ease the pressure on the economy for some time, but it ends in May; after that comes the Parliamentary election, preceded by promises and followed by a new dispensation. On another front, Mongolbank is taking steps, supported by the Finance Ministry, to remove Mongolia from the ‘gray list’ of FATF. What an interesting year 2020 is going to be!

In May 2017, the IMF approved a $5.5-billion financial programme. Of this $2 billion was spent on extending Mongolbank’s swap agreement with People’s Bank of China. So far, $1.1 billion of the remaining $3.5 billion has been disbursed. The rest will come only after a fresh review by the IMF. There have been distinct gains from the IMF programme: fiscal consolidation has been effected, a sense of fiscal discipline has been imposed, the financial system, particularly banking, has been brought closer to international standards, and forex reserves are at a historic high. The Finance Ministry included only MNT1.3 trillion of the IMF money in this year’s budget. If after review or for any other reason, the IMF does not pay the remaining amount, the programme would effectively end. There are indications that the Ministry is ready for that eventuality. That would shut out one source of funds with low interest rates and long maturity periods.

The situation will be fluid until we know how the coronavirus problem plays out. Lower exports are never good but we have enough foreign exchange to meet nine months’ import costs. There would be some enforced savings, too. With no coal export, there would be no outflow of foreign currency to pay for coal transport, and with a travel ban in place, fewer Mongolians would spend money on visits abroad. And since necessity is the mother of invention, maybe Mongolia would find a way out of its over-reliance on commodity exports or, at least, build a railway immediately and develop other infrastructure that would help us meet such unexpected challenges. The need for expanding our domestic manufacturing base was highlighted by the fact that we did not produce enough face masks to meet our needs. Fortunately, we are self-sufficient in flour and meat, and restriction on imports from China would force us to pay more attention to farmers and herders. There are now masks everywhere, but they cannot hide the fact that our economy is way too much dependent on coal export, and is ill-prepared to withstand an external shock.